Understanding the GST System In India

Goods and Services Tax came into effect from 1st July 2017 in India. It replaced multiple existing indirect taxes which were previously levied by the Central and State government in the country. In this article, you will learn about the existing GST system in India, who regulates it, what GSTN is, etc.

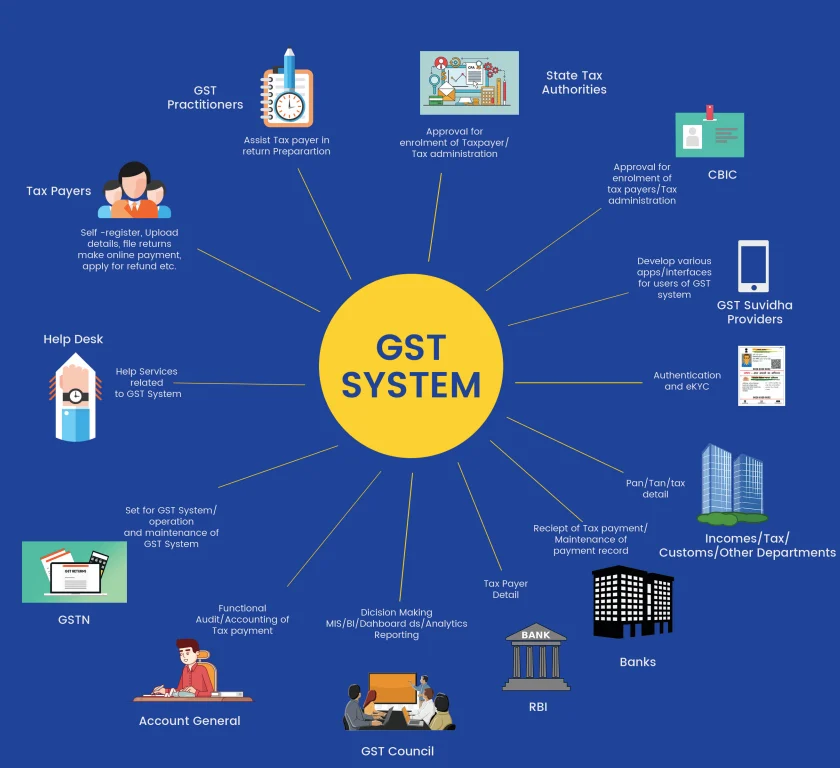

Who is a GST Practitioner?

A GST Practitioner is a registered person, who is authorized/ have been approved by the GSTP to furnish information on his behalf, to the government.

GSTN will be provided a separate user ID and password to GSTP to enable him to work on behalf of his clients without asking for their user ID and passwords.

They can do all the work on behalf of taxpayers as allowed under GST Law.

A taxpayer may choose a different GSTP by simply unselecting the previous one and then choosing new GSTP on the GST Portal. The tasks performed by a GST practitioner include the following -

- Registration: Assisting with GST registration applications, amendments, or cancellations.

- Returns: Preparing and filing monthly, quarterly, or annual returns like GSTR-3B, GSTR-1, and GSTR-9.

- Refunds/Payments: Filing refund claims or making tax payments for registered persons.

- Authorized Representation: Representing taxpayers before GST officers, appellate authorities, or the Tribunal.

What is the role of CBIC?

Central Board of Indirect Taxes and Customs (CBIC) is a part of the Department of Revenue under the Ministry of Finance, Government of India. It deals with the tasks of policy formulation concerning the levy and collection of Customs & Central Excise duties and Service Tax, prevention of smuggling, and administration of matters relating to Customs, Central Excise, Service Tax, and Narcotics to the extent under CBEC’s purview. CBIC is playing an active role in the drafting of GST law and procedures, particularly the CGST and IGST law, which will be the exclusive domain of the Centre. Apart from this, the CBIC has successfully prepared itself to meet the implementation challenges, which are quite formidable.

CBIC would be responsible for the administration of the CGST and IGST law. In addition, CBIC continues to administer the excise duty regime for the collection and levy of central excise duty on 5 specified petroleum products and tobacco products.

What is the role of GST Suvidha Providers(GSP)?

A GST Suvidha Provider (GSP) is a key initiative under the Goods and Services Tax (GST) framework. The Government of India has appointed 34 GSPs to simplify compliance for taxpayers.

GSPs develop user-friendly applications that enable seamless communication with the Goods and Services Tax Network (GSTN), a non-profit organization established on 23 March 2013 to manage GST data for both state and central governments.

Using GSP platforms, companies can file GST returns, with the data transmitted directly to the GSTN. GSPs play a crucial role in helping taxpayers maintain GST compliance efficiently.

GSP is a person who provides the facility for GST compliance online. There are a number of GSPs which are providing GST compliance services to the taxpayers. We can say that GSPs act as a bridge between the GST Network and Application Service Providers. Although any data cannot be read or modified by GSPs. However, to help taxpayers in their filing, GSPs can use the APIs given by the Goods & Services Network to manage enhanced systems.

What is the role of banks under GST system?

Banks play a vital role in the whole process of GST collection and maintenance. The branch of remitter bank is required to ensure that the correct CPIN is entered in the NEFT / RTGS message and also inform UTR to the taxpayer and Transfer the amount indicated in the NEFT / RTGS message to RBI. Banks also provide the facility of paying GST through NEFT, challan, and includes functions like-

a) Accepting the payment through the customized GST software/screen in its system only.

b) Provide an acknowledgment to the taxpayer

c) Send the instrument (if pertaining to another bank) to the clearinghouse for realization and record the result in the IT system as and when the response is received.

d) Credit the realized amount into either GST pool account, if so, maintained by the authorized bank (in its e-FPB) and after that transfer such amount into the individual tax head accounts as shown in the challan or to directly credit the amount to the respective government’s account.

What is RBI’s role in Goods and Service Tax regime?

The Reserve Bank of India (RBI) serves as the aggregator for accounting all GST collections into respective government accounts. Agency banks that collect GST payments for challans generated on the GST portal report these collections to the RBI for settlement.

Additionally, the RBI enables taxpayers to directly pay GST into government accounts using NEFT/RTGS payment options available on the GST portal, ensuring a streamlined process for GST payments.

What is the GST Council?

Goods and Services Tax Council empowers the president of India to constitute a joint forum of the center and States, namely the Goods and Services Tax Council. Provisions relating to GST Council came into effect on 12th September 2016. The president constituted the GST council on 15 December September 2016. GST Council is allowed to make recommendations to the Union and the states on matters like-

I. The taxes, cesses, and surcharges levied by the union, the states, and the local bodies which may be subsumed in the goods and services tax.

II. The goods and services that may be subjected to or exempted from the goods and services tax.

III. The goods and services tax Council shall determine the procedure in the performance of its functions.

What is GSTN?

GSTN, or Goods and Services Tax Network, is a non-profit, non-governmental organization that provides shared IT infrastructure and services to central and state governments, taxpayers, and other stakeholders.

GSTN facilitates key services such as registration, return filing, and payments for taxpayers, serving as the primary interface between the government and taxpayers under the GST system.

What is the Role of Account General under GST System?

The following functions will be performed by the Accountant General of State:

a) Every Account General will receive daily and monthly Put Through Statements from CAS, RBI.

b) They will also receive verified Datewise Monthly Statements (DMS) from e-PAOs and e-treasuries of the State, respectively.

c) The reconciliation of both types of data will be carried out by the Account General.

Who is a Taxpayer under GST System?

Every person having a turnover above Rs.20 Lakhs is required to self register under GST. All the person registered under GST are required to –

- Self-register

- Upload details

- File returns and make the online payment

- Apply for refund etc

Find filing GST returns complicated, or don’t have enough time? Don’t worry! Our CAs are here to help you with GST return filing. Get expert guidance and experience seamless and hassle-free GSTR filing so that you can focus on what matters most. Book an online eCA Now!

Frequently Asked Questions

Q- Why do we need GST?

The primary goal of implementing GST is to eliminate double taxation, or the 'tax on tax,' that occurs throughout the supply chain, from manufacturing to consumption.

Q- How is GST charged?

Under the GST system, tax is applied at every point of sale. For intra-state sales, both Central GST (CGST) and State GST (SGST) are charged, while inter-state sales are subject to Integrated GST (IGST).

Q- What are Dual Goods and Services Tax Structures?

Dual GST is a system where both the central and state governments impose GST on a shared tax base. For intra-state supplies, Central GST (CGST) and State GST (SGST) are levied, while Integrated GST (IGST) applies to inter-state supplies. The IGST is then divided between the center and the states.

Q- What is the limit imposed on GST?

The GST threshold turnover determines whether registration is required. Individuals exclusively supplying goods with an annual turnover up to ₹40 lakhs are exempt from GST registration. However, the limit is ₹20 lakhs for special category states and ₹10 lakhs for hilly states, including Jammu and Kashmir.

Q- Is it necessary for all traders to register under the GST?

Not all traders need to register under GST. Registration is mandatory for traders whose aggregate turnover exceeds the threshold limit or those engaged in specific activities such as inter-state supplies, reverse charge tax payments, tax deduction at source, e-commerce operations, or supplying certain notified goods or services.