What is Input Credit under GST ? How to Calculate & claim it?

GST was implemented by subsuming various indirect taxes like VAT, central sales tax, octroi, excise duty, service tax, etc. This was primarily introduced with the objective of avoiding the cascading effect of taxes. To overcome this, the system of Input tax credit was introduced.

Input Tax Credit means reducing the tax liability on outputs by the amount of taxes paid on inputs. It is a procedure to avoid charging tax on the tax already paid on inputs. This article explains what is input tax credit under GST, how to calculate the input tax credit, and claim it.

What is Input Tax Credit?

ITC or Input Tax Credit refers to the tax paid on the purchases for the business that can be claimed as a deduction at the time of paying tax on output tax.

Input Tax Credit (ITC) allows businesses to claim a deduction for the tax paid on purchases against the tax payable on sales.

When you purchase goods or services from a registered dealer, you pay tax on the purchase. On selling those goods or services, you collect tax from the buyer. The tax paid on purchases is adjusted against the tax collected on sales. The remaining tax liability (output tax minus input tax) is then paid to the government.

Say, a business purchased the raw material to manufacture its final product for Rs 100. On such purchases, he is liable to pay GST at a certain percentage, say @18%, i.e., Rs 18 (input tax) in this case. Moreover, on selling such products after value additions say for Rs 200, they collect certain taxes presumed @28%. This is known as payment of output tax amounting to Rs 56 in this case. Under GST, the taxpayer is required to pay only the differential amount of tax, i.e., (output tax liability payable - input tax already paid) with the government. Therefore, the ent payable amount will be Rs.56-18 = Rs.38, and not the entire amount collected, i.e., Rs.56.

Conditions for Claiming ITC

The prerequisites for taking the input tax credit are as follows:

- The dealer must have a valid tax invoice.

- The goods or services must have been received.

- The recipient must file GSTR-3B.

- The supplier must have paid the tax to the government.

- The recipient must pay the invoice or debit note amount within 180 days from the invoice date.

- ITC can be claimed only after receiving the last lot or installment.

- ITC can only be claimed for taxable supplies used in furtherance of business.

- No ITC is allowed if depreciation is claimed on the tax component of a capital good.

-

ITC must be claimed within the earlier of:

- 30th November of the year following the financial year in which the document was issued.

- The date of filing the annual return.

- ITC claims in GSTR-3B must align with details in GSTR-2B, as per CGST Rule 36(4).

- ITC cannot be claimed by individuals under the composition scheme.

What can be Claimed as ITC?

ITC can only be claimed for business purposes by persons registered under GST. ITC is not available for goods and services exclusively used for -

- Personal Use

- Exempt Supplies

- Supplies for which ITC is not available under CGST section 17(5)

What Cannot be Claimed as Input Tax Credit?

Section 17(5) of the CGST Act specifies an exclusion list of transactions and businesses that are not eligible for Input Tax Credit (ITC). ITC cannot be claimed on these items, while all others remain eligible.

Instances of Ineligible ITC -

- ITC cannot be claimed for motor vehicles used for personal purposes except when used for resale, commercial activities, or mandated cab services.

- ITC is ineligible for expenses on catering, health services, and similar items unless these services are legally required.

- Club or gym memberships do not qualify for ITC.

- Health and life insurance are excluded unless mandated by the government.

- ITC cannot be claimed for costs incurred in constructing immovable property.

- ITC is disallowed for goods that are lost, destroyed, damaged, or given away as gifts.

Time Limit to Claim Input Tax Credit Under GST

Input Tax Credit (ITC) can be claimed in GSTR-3B within the time limit specified under GST law. The deadline to claim ITC for an invoice or debit note issued in a financial year is the earlier of:

- 30th November of the year following the financial year.

- The date of filing the annual return for that financial year.

Points to Note:

Although the deadline is 30th November, ITC is reported in GSTR-3B. Hence, the due date for filing GSTR-3B of October in the following year (20th November) is considered the practical deadline without incurring a late fee.

If GSTR-3B for October is filed after 20th November but before 30th November, ITC can still be claimed, but a late fee will apply.

Documents Required for Claiming ITC

Here are the documents that you need to furnish to claim ITC -

- Tax invoice issued by the supplier.

- A bill of supply when the total amount is less than Rs.200 or when a reverse charge mechanism is applicable.

- A debit note issued by the supplier, if applicable.

- A bill of entry is issued by the customs department.

- A credit note or invoice from the ISD.

Special Cases of Input Tax Credit (ITC)

ITC for Capital Goods

Capital goods are assets like machinery, equipment, or buildings used in business operations to produce goods or services. ITC is available for capital goods, except in the following scenarios:

- When capital goods are exclusively used to produce exempt goods.

- When capital goods are used solely for personal purposes.

- When depreciation is claimed on the tax component of the capital goods.

ITC on Job Work

Job work involves a principal manufacturer sending goods to a job worker for further processing. For example, a shoe manufacturer may send semi-finished shoes for sole fitting.

- The principal can claim ITC on tax paid for goods sent, either from their premises or directly from the supplier.

- To qualify for ITC, the processed goods must be returned within one year (or three years for capital goods).

ITC Provided by Input Service Distributor (ISD)

An ISD is an entity that receives input services and distributes the related ITC across different units of a company.

- The ISD consolidates ITC from all purchases and allocates it to branches based on their tax liabilities.

- Distribution occurs under specific tax categories, such as CGST, SGST/UTGST, IGST, or cess, ensuring each unit receives the appropriate credit.

ITC on Transfer of Business

During business mergers or transfers, the ITC of the existing business can be transferred to the new business.

- This process maintains continuity in tax credits and ensures smooth business operations during structural or ownership changes.

Utilization of Input Tax Credits

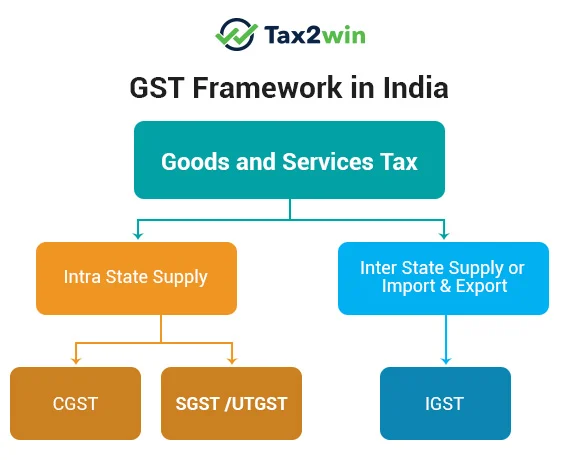

There are three types of taxes available under GST, i.e., CGST, SGST, IGST. Moreover, the same is available to take the credit on input. Their credit can only be set off for specific purposes. The following are the restriction on utilizing credits of various input taxes available:

- IGST credit,

- First, the credit is available to set off against IGST credit,

- Then for balance (if any) set off with CGST and then SGST/UTGST.

- CGST credit,

- It is to be utilized against IGST and

- then balance with CGST,

-

SGST Credit,

- It can be utilized to set off for IGST, and

- Then the balance for SGST/UTGST .

ITC treatment in case of input goods and services

The input tax credit concerning inputs or input services which are being

- partly used for business and

- partially for other purposes or

- being partly used for effecting taxable supplies, including zero-rated goods and services and

- partly for changing exempt supplies shall be attributed to the purpose of business or

- for influencing taxable supplies in the following manner, namely:-

Step 1: First, we need to calculate common credit

| Total input tax related to inputs and input services in a tax period | T |

|---|---|

| Less: Input tax on inputs and input services that are intended to be used exclusively for a nonbusiness purpose | (T1) |

| Less: Input tax on inputs and input services that are intended to be used exclusively for exempt supplies | (T2) |

| Less: Input tax which is ineligible for a tax credit (Blocked credits) | (T3) |

| ITC Credited to Electronic Credit Ledger | C1 |

| Less: Input tax on inputs and input services that are intended to be used exclusively for taxable supplies, including zero-rated supplies | (T4) |

| Common ITC available for apportionment | C2 |

Step 2: Now we will calculate the credit attributable to exempt supplies (Ineligible credit) by the apportionment of the common credit

D1= (E/F) x C2

Where,

D1 = the amount of input tax credit attributable to exempted supplies

E = The aggregate value of exempt goods or services during the tax period

F = The total turnover of the state of the registered person during the tax period

C2 = Common credit available

Step 3: After that, we need to calculate the amount of the credit attributable to nonbusiness if common inputs and input services are used partly for business and partly for nonbusiness purpose

D2 = 5% of C2

D2 = the amount of input tax credit attributable to nonbusiness purpose

Step 4: Now we will calculate the total eligible ITC

C3 = C2 – (D1 + D2)

C3 = the eligible input tax credit from the common credit

Note: The amount equal to the aggregate of D1 and D2 shall be included in the registered person‘s output tax liability.

How to Claim Input Tax Credit?

Given below are the steps that you need to follow to claim input tax credit -

- Step 1. Report all eligible ITC in the GSTR-3B form, including credits from imports, reverse charge supplies, ISD invoices, and other qualifying purchases.

- Step 2. If any inputs, services, or capital goods are used for non-business purposes or exempt supplies, reverse the proportionate ITC accordingly.

- Step 3. Deduct the reversed ITC from the total available ITC to determine the net ITC you can claim for the tax period.

- Step 4. Remove ITC on items restricted under Section 17(5) of the CGST Act, such as expenses related to employees (e.g., travel, food, etc.).

- Step 5. Enter the final net ITC amount in the appropriate section of GSTR-3B and submit the return.

Earlier, taxpayers could claim full ITC based on their records. However, Rule 36(4) now limits provisional ITC claims to 105% of the ITC reflected in GSTR-2B.

This restriction does not apply to ITC on:

- Imports of goods.

- Input service distributors (ISD).

- Transactions under the reverse charge mechanism (RCM).

Want to claim your input tax credit but confused about how to do it? If you are among those who find taxes complicated, getting professional help is the solution for you. Our experts can help you with both GST return filing and also solve your GST-related queries. Book an online CA now!

Frequently Asked Questions

Q- Who is eligible for ITC in GST?

A registered taxable person or entity can claim an Input Tax Credit (ITC) for the taxes paid on business-related purchases and expenses.

Q- Can we claim ITC on hotel stays?

Yes, ITC can be claimed on GST for hotel services if the hotel charges SGST and CGST and is located in the same state as the business traveler or the company. However, ITC on in-house restaurant charges (with a 5% GST) is not allowed.

Q- Is ITC refundable?

Yes, unutilized ITC can be refunded under specific conditions, such as in cases of Inverted Duty Structure (IDS). To apply for a refund, you need to complete Statement 1 and Statement 1A of Form GST RFD-01A and confirm that you haven't claimed any tax drawbacks.

Q- How to calculate ITC?

To determine the Input Tax Credit (ITC) for a tax period, follow these steps:

- Add up the GST paid on all eligible purchases during the relevant tax period.

- Determine which inputs qualify for ITC based on GST law.

- Multiply the total eligible GST paid on purchases by the eligible input percentage to calculate the total ITC.

- Subtract the calculated ITC from the GST payable on sales for the tax period to determine the net GST liability.

Q- What is meant by input tax?

Input tax includes the following taxes:

- CGST (Central Goods and Services Tax)

- SGST (State Goods and Services Tax)

- IGST (Integrated Goods and Services Tax)

- UTGST (Union Territory Goods and Services Tax)

- Taxes under the Reverse Charge Mechanism (RCM)

However, it excludes taxes paid under the composition scheme.

Q- What are the benefits of ITC?

ITC helps reduce the tax burden by allowing businesses to offset input taxes against output tax. This mechanism improves cash flow and enhances profitability, as businesses can reduce their overall tax liability.

Q- What is the time limit for claiming ITC?

The time limit for claiming ITC is earlier of the following dates -

- 30th November of the following financial year

- The date of filing annual returns.