How to File ITR-U Using Tax2win?

Tax2win offers two types of ITR filings:-

DIY (Self-filing)

DIY (Self-filing)- If you have a little bit of knowledge about taxes, entering some basic details will let you file the ITR within 4 minutes. Tax2win DIY platform is AI-integrated, hence it will auto-select the right ITR form for you itself and thus makes filing super-easy for you.

If you are wondering how to file an ITR with Tax2win, here are some simple steps you need to follow -

Step 1: Either sign in to the tax2win website using your existing credentials or sign up to the portal and create an account. You can do self-filing only in the case of income from salary, business, and capital gains.

Step 2: After logging in, a table consisting of all the possible sources of income opens. You need to select the income sources that you have. Based on your sources of income, Tax2win’s DIY ITR filing system selects the applicable ITR form automatically.

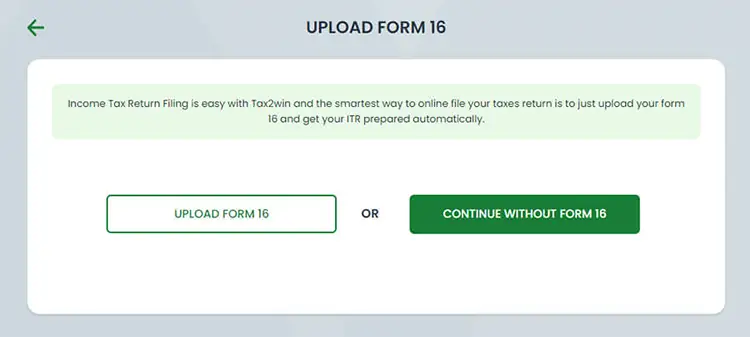

Step 3. You need to upload Form 16. In case you don’t have Form 16, you can simply skip the option and proceed further.

Step 4. Select the F.Y. for which you want to file the ITR and enter the PAN Details and DOB. (If you don’t have a registered account with the Income Tax Department, you will receive an OTP and a new account will be created.). You can also choose if you want our DIY software to fetch your personal details and get data pre-filled.

Step 5: Enter a few basic details in the next step. Some of it is pre-filled from the Income Tax Department’s database. Remember to cross-check the information available. As shown in the image given below, you have to enter your personal details like name, email ID, date of birth, father’s name, gender, etc.

Step 6: In the next step, you have to provide your address details and employer category. You can refer to the image below to understand this better.

Step 7. In the next step, you have to fill in your employment details. The standard deduction is applied automatically in the case of salaried employees. As shown in the image below, you have to enter your gross salary/CTC, exempted allowances like HRA, LTA, gratuity, net salary, and standard deduction and professional tax under section 16. Note that if you have uploaded Form 16, your employment data will be pre-filled in the ITR Form. All you have to do is verify the information and proceed to file ITR.

Step 8: Enter the details of the investment made during the year to calculate the applicable deductions. You have to enter details of investments in PPF, LIC, PF, housing loan, FDR, NSC, tuition fees, premiums paid to the annuity, and other 80C deductions. Also, you can claim deductions like 80D, 80CCD (1B), 80G, etc.

Step 9: In this step, you are required to enter your bank details. Enter your IFSC code, name of the bank, account number, and Aadhaar details. As per government law, it is mandatory to show all the bank details. You can select one account as the primary account. Remember, you will get a tax refund in your primary bank account.

Step 10: If you have your Form 26AS, simply upload it; otherwise, enter the details manually. Enter your salary details, previously paid taxes like advance tax/self-assessment tax, tax paid on updated return, TDS paid on income except salary, TDS on rental income, and TCS.

Step 11: Select the return filing type as ITR-U. If you have not filed your ITR for this year, select “not filed.” If you have already filed your ITR for this year, select “under section 139(1) and fill in the details of the ITR filed and click on continue.

Step 12: Based on the information given by you in the previous sections, the software automatically computes your tax liability using both the old and the new regime. You can compare both regimes and select the one that is more beneficial for you.

Step 13: Now, you can see your total tax due along with an option to pay your income tax online through the income tax portal. You can also pay your taxes offline using the income tax challan method. Click on continue.

Step 14: Now, you are ready to file ITR-U. You can either download the JSON file and upload it to the Income Tax Department or get an eCA to file your ITR-U, if you have any doubts.

File ITR Now

The second way through which you can file ITR on Tax2win is:-

Expert-Assisted ITR Filing

Step 1. Click on Hire eCA Now.

Step 2. Select the relevant options from the below steps.

If you have any income from outside India -

If you have any salary income and from how many employers -

Select whether you have any business or professional income -

Select whether you own a house -

Select if you have any capital gain income -

Step 3. Based on your financial situation, our AI-integrated software will automatically aseletc the most suitable plan. You can simply click on pay now to pay a small fee and you will receive a call from our tax experts who will then file your ITR accurately.

Book Your eCA Now