What is income from house property?

Any income arising from house property, i.e., rental income, is considered ‘Income from House Property’ under the Income Tax Act. The house property here means a house, building, office, and warehouse. There are different ways to calculate taxable income from house property based on its type - self-occupied and let out.

Self-occupied property is the one that is used for one’s residential purpose. And a let-out property is the one that has been rented out to a tenant even for a few months. In the next step, we will guide you about how to calculate taxable rental income from a let-out property and file your ITR accurately.

Details to be Filled in ITR-1

Personal Details of an Individual

You need to enter your complete name, gender, date of birth, PAN, and father’s name. You must also enter their postal address, email address, and mobile number.

Upload Form 16 for Income From Salaries

You must declare your income from your salary, including the following details -

- Name of the Employer

- Type of the Employer

- TDS on salary

- Break up of income from salary

- TAN of the employer

Details of Other Income

Enter the details of your income from other sources like interest, dividends, winnings from the lottery, online gaming, etc. In other words, any income that does not fall under capital gains or business/profession

Details of House Property

If you have a self-occupied house property, you must mention the following details -

- Interest on loan paid/payable on the housing loan on the property.

- Interest paid during the pre-construction period.

- Address of the house property

- For a co-ownership, the name, PAN and percentage of share of co-owners in his property.

In case of a property let out on rent, you need to furnish the following details -

- Annual rent received/receivable

- Municipal tax paid

- Name and PAN of the tenant.

- Interest paid/payable on a housing loan on property

- Pre-construction period interest

- Address of property and other details of the co-owners of the property

- Details of tenants such as name, PAN and TAN.

Details of Tax Deductions

- Municipal Taxes Paid

- Co-ownership Details (Name, PAN, and share percentage) to ensure tax liability applies only to your share.

- Interest on Housing Loan (up to ₹2,00,000).

- Additional Deduction under Section 80EEA (up to ₹1,50,000) if conditions are met.

- Standard Deduction of 30% on rental income (after deducting municipal taxes) for maintenance.

- No additional deductions are allowed for expenses like sweeping, painting, or renovation against rental income.

How to e-file ITR 1 with rental income from house property?

Once you have calculated the taxable income, follow these steps to file your ITR-1 with rental income from house property.

Step 1. Log in to the e-Filing portal using your User ID (PAN) and Password.

Step 2. Click on e-File > Income Tax Returns > File Income Tax Return.

If your PAN is inoperative, you’ll see a warning. Click ‘Link Now’ or ‘Continue’.

Step 3. Select Assessment Year 2024-25 and Mode of filing: Online, then click Continue.

Step 4. If you have a saved return, choose ‘Resume Filing’. If you want to start fresh, select ‘Start New Filing’.

Step 5. Select your applicable status (Individual, HUF, etc.) and click Continue.

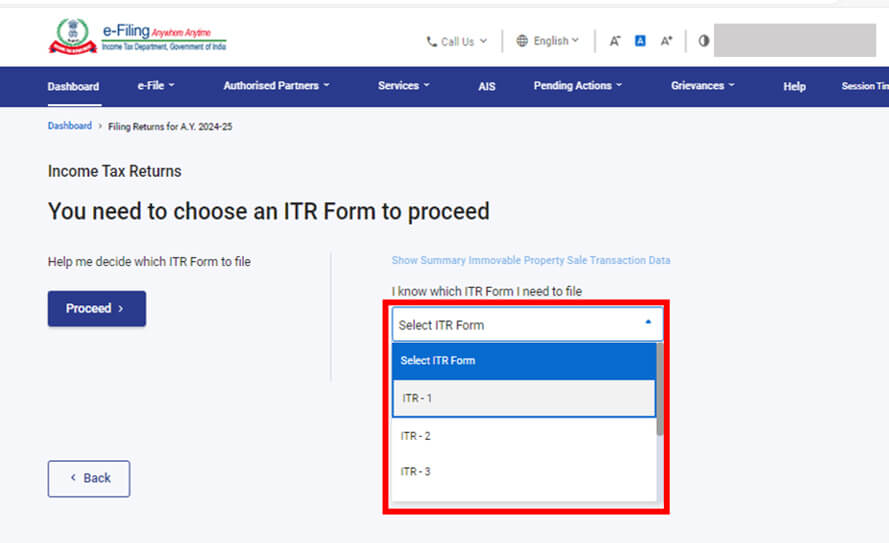

Step 6. If you know which ITR form to file, select it. If unsure, select ‘Help me decide’, answer the questions, and let the system recommend the correct form.

Step 7. Review the list of required documents and click ‘Let’s Get Started’.

Step 8. Select the applicable checkbox for your reason for filing ITR and click Continue.

Step 9. The New Tax Regime (default) is pre-selected. If you want to opt out, select ‘Yes’ under the Personal Information section. Review and edit pre-filled details, then Confirm each section.

Step 10. Enter income and deductions in the respective sections. After completing all details, click Proceed.

Step 11. If tax is payable, you will see a tax computation summary. Choose ‘Pay Now’ (recommended) or ‘Pay Later’. If you delay payment, interest may apply.

Step 12. If no tax is payable or if a refund is due, click ‘Preview Return’.

Step 13. If you chose ‘Pay Now’, you’ll be redirected to the e-Pay Tax service. Complete payment and return to the ITR filing process.

Step 14. Click ‘Preview Return’, check all details, select the declaration checkbox, and click Proceed to Preview.

Step 15. Click ‘Proceed to Validation’. If there are errors, correct them before moving ahead.

Step 16. Click ‘Proceed to Verification’ and e-Verify your return.

Step 17. Choose your preferred verification method (Aadhaar OTP, Net Banking, or DSC) and click Continue. If you choose ‘e-Verify Later’, you must verify within 30 days to complete the filing.

Step 18. Once successfully verified, your ITR is filed.

")